Given the ever-increasing demands for efficient and flexible financial planning in public administration, the transition from traditional budgeting to a modern budget management system is becoming increasingly important. However, with the introduction of S/4HANA at the latest, this transition has become essential, as traditional budgeting will no longer be supported. The transition to the modern budget management system (BCS) will not only enable adaptation to current requirements but also lay the foundations for a long-term, sustainable financial strategy that meets the changing needs of public administration.

How does traditional budgeting differ from a budget management system?

The following table compares the features of the two budgeting systems:

Most of the functions of traditional budgeting have been retained in the Budget Control System (BCS). For example, tolerance limits can still be set, either as absolute values or as percentages. Provisional budget postings also remain. The account assignment elements from traditional budgeting have been carried over into BCS and supplemented by the budget programme. The budget programme offers a further option for classifying expenditure.

| Function | Traditional budgeting | Budget management system |

| Hierarchy of budget values | Yes | No |

| Budget categories | Yes | Yes (Ledger) |

| Budget types | Yes | Yes (formerly a budget sub-type) |

| Budget sub-types | Yes | Not applicable |

| Budgeting process | No | Yes (previously known as ‘budget type’) |

| Budget approval | Yes | Yes |

| Kontierungselemente für die Budgetierung | AccouFund centre, fund item (optional), functional area (optional) | Funds centre, Commitment item, Fund (optional), Functional area (optional), Budget programme (optional) |

| tolerance limits | Yes | Yes |

| Provisional budget entries | Yes | Yes |

| Definition of key performance indicators | No | Yes |

| Budget Structure Plan | From one year old and upwards | Per year |

| Grant management | No | Yes |

Unlike in budgeting, account assignment is not carried out directly. Instead, it is performed via the department or other account assignment elements. Whilst hierarchies for funds centres and commitment items could still be used in traditional budgeting, this option is no longer available in BCS, and distribution or totalling functions are no longer possible. However, hierarchies can still be used for reporting purposes.

Whereas in traditional budgeting only the three budget categories – payment budget, commitment budget and financial plan – were available, in BCS you can also define your own budget categories via ledgers. The budget categories from traditional budgeting are already included as ledgers in the standard system.

The significance of budget types in the budget management system

The budget type in classic budgeting (original, transfer, etc.) corresponds to the budgeting transaction in BCS. The term ‘budget type’ continues to be used in BCS and corresponds to the budget sub-type in classic budgeting.

The switch to BCS also makes it possible to define key figures derived from aggregated transaction data in user-specific data sources. One example is the calculation of the remaining budget for carrying forward budget data to the next financial year. The PSM-GM grant management module can only be used in conjunction with BCS, which is why the switch is essential for its use.

How can a migration to the budget management system be carried out?

It should be noted at the outset that, due to the variety of budgeting scenarios within the public sector, SAP cannot provide a one-size-fits-all migration strategy that applies to all customers. Rather, a thorough analysis of the customer’s systems is required in order to meet all requirements. In principle, data migration during the transition to BCS can be carried out in two ways:

Total-based migration: Individual budget documents are not migrated. Instead, only the totals of the budgets from classic budgeting are transferred to BCS.

Document-based migration: In this case, the complete documents are transferred to BCS.

The type of migration used depends on several factors, including the timing of the migration.

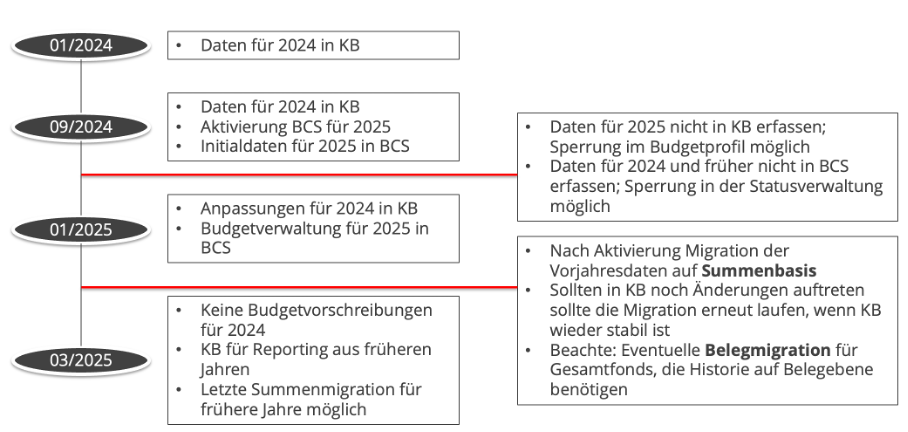

Migration at the end of the financial year

When migrating at the end of a financial year, all data for the current financial year is recorded in classic budgeting. At the start of the following year, budget management then takes place via BCS, although classic budgeting can still be used for reporting purposes relating to previous years. Once BCS has been activated, data from previous years is migrated on a summary basis. It should be noted that any change made in classic budgeting requires a new migration to be carried out. It is also necessary to check whether a complete document history is required for total funds, as in this case an additional document migration must take place.

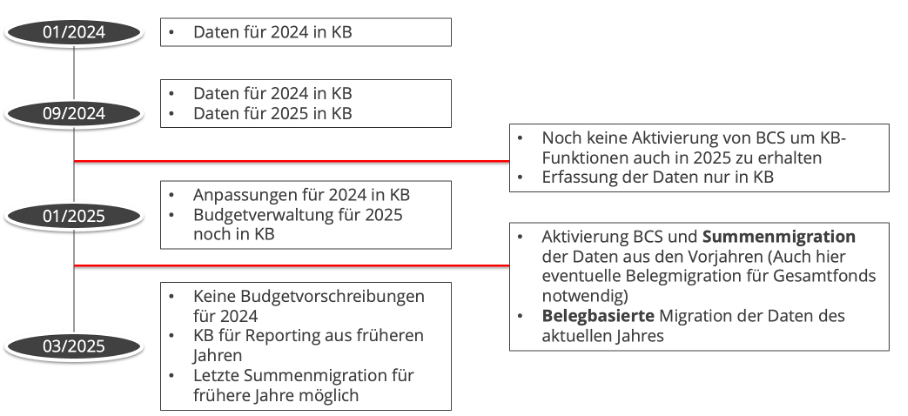

Migration during a financial year

Migration during a financial year is carried out by continuing to enter data for the year in question using the traditional budgeting process, so that the functions for that year remain available. When BCS is activated, a summary migration of the closed previous years takes place. For the data of the current financial year, however, a document-based migration is performed to ensure that it is fully available.

When should the migration take place?

In conclusion, it can be said that a migration to S/4HANA offers many benefits and new features even prior to the full S/4HANA transformation. Given the complexity and unique nature of individual structures and processes, it is only possible to determine exactly when a migration should take place and which features are appropriate in each specific case following a thorough, comprehensive analysis.