What is ViDA and why now?

Tax fraud, complicated reporting requirements, and differing national regulations in cross-border trade mean that preparing reports is becoming increasingly complex and prone to errors. These circumstances mean that the current VAT system is reaching its limits and causing enormous losses: according to the European Commission, these amounted to around €93 billion within the EU in 2020.

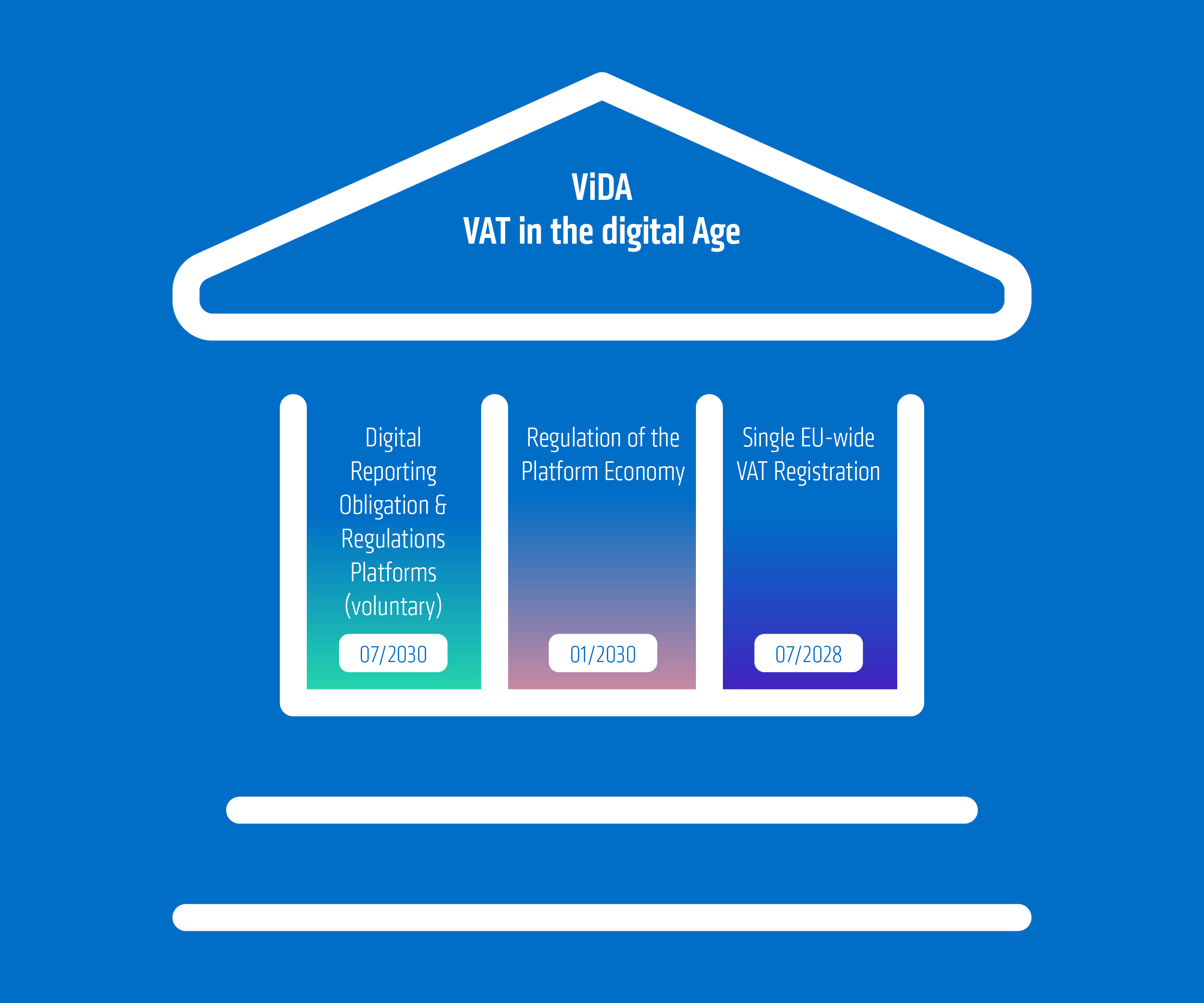

This is precisely where the EU wants to start with ViDA – “VAT in the Digital Age” – and fix this problem. The goal is clear – a modernization package based on three pillars: digital reporting requirements, platform economy, and uniform VAT registration. These pillars form the basis for a modern, digital, and uniform VAT system that is intended to ease the burden not only on authorities but also on businesses.

An overview of ViDA’s 3-pillar model

PILLAR 1: Digital Reporting Requirements

From July 1, 2030, companies will be required to use electronic invoices for cross-border B2B transactions within the EU. Read more about this in another blog post here. This rule may already apply in some countries from 2028. The central function here is real-time reporting, which will replace summary reporting in the future. A uniform, structured format will be used throughout the EU for the transmission of transactions.

The advantages for companies:

- More automation, fewer manual processes

- Lower risk of errors and greater transparency

- Lower costs and less administrative effort in the long term

Challenges at the start:

- Adaptation of IT systems and data quality

- Employee training

- Stricter data protection and security requirements

In short: Reporting will become easier in the future, as it can be standardized and, depending on the tool used, automated. The result will be long-term relief for companies and authorities alike.

PILLAR 2: Platform economy (VAT treatment of the platform economy)

The second ViDA pillar will come into force on January 1, 2030, and deals with digital platforms that mediate goods or services. Well-known examples can be found on platforms for short-term rentals of premises, transport services, or online marketplaces. These platforms must be clearly assigned for tax purposes in order to process cross-border transactions transparently.

If the actual provider does not pay sales tax, the platform steps in instead. In these cases, the platform is considered a “fictitious supplier” and pays the sales tax. There is also a flexible transitional arrangement here: if it is a small business, the platform assumes the role of tax debtor.

Advantages for companies:

- Greater clarity and legal certainty regarding sales tax liability

- Lower liability risk thanks to clear regulations

- More accessible market entry for small businesses

Challenges for companies:

- Adaptation of IT systems and processes to the new requirements

- Additional reporting requirements for platform sales

- Increased complexity due to national exemptions and transitional solutions

The aim of this pillar is to close the tax loopholes in digital business models and create a much fairer competitive environment in the EU single market.

PILLAR 3: Single VAT registration

From July 1, 2028, central VAT registration will become mandatory. As a result, companies will rarely have to register separately in several EU countries. Instead, they will be able to do so via a single digital portal. The basis for this is the existing One-Stop-Shop (OSS) procedure, which will be expanded for the new use, for example through Import One-Stop-Shop (IOSS).

Advantages for companies:

- Less administrative effort due to the elimination of multiple registrations

- Digital portal as a central point for tax returns

- Less effort for reporting and compliance, as well as better predictability

- Easier cross-border trade thanks to standardized processes

Challenges in practice:

- Adaptation of IT systems and processes for central registration

- Traditional national and new EU regulations during the transition period

- Consistency and accuracy of data are essential for a sound database

It is clear that the goal is to simplify compliance for companies while at the same time providing authorities with greater control through the central database.

SAP Document & Reporting Compliance as a possible solution

At first glance, this sounds like a lot of effort, but there are already solutions that make the transition much easier and can be implemented right now. One example is SAP Document & Reporting Compliance (SAP DRC).

With SAP DRC, electronic outgoing invoices, advance sales tax returns, and other legally required reports can be generated automatically and sent directly to the relevant authorities. What makes SAP DRC special is that, depending on the country, the local legal reports are included in the standard version and a connection to the respective authorities is set up directly. This enables companies to position themselves well at an early stage and work in compliance with ViDA, without any manual interfaces or media breaks.

In terms of the changes brought about by ViDA, SAP DRC is particularly helpful in complying with the first pillar. Here, outgoing invoices can be automatically transmitted to the relevant authorities without the need for further manual steps.

Conclusion: Act now!

ViDA brings a breath of fresh air and considerable momentum to the European tax landscape. The goal is a digital system that makes taxes more efficient and transparent for both companies and authorities.

Like other digitization projects, ViDA requires investment in systems and processes, as well as in expertise. In addition to legal certainty, companies also gain a clear competitive advantage if they act early.

Particularly in the first pillar (digital reporting requirements), a solution such as SAP Document & Reporting Compliance (SAP DRC) can make a decisive difference. Instead of manually maintaining interfaces and reports, companies benefit from automated, ViDA-compliant processes. These are already available today.

Our appeal: Check your systems and prepare your teams. Use modern tools such as SAP DRC to prepare yourself optimally for ViDA. Don’t put off the issue – act today. With adesso business consulting, you have an experienced partner at your side to support you with the technical implementation. Our experts will help you analyze your existing system landscape, implement SAP DRC in a targeted manner, and prepare your team for the new reporting requirements. This will not only make you compliant tomorrow, but also give you a competitive edge. We would be happy to support you in this transformation. Feel free to contact us – the adesso bc team will provide you with expert guidance on your way to the next level of the tax world.