With the introduction of S/4HANA, a new FI-AA solution is being implemented. This differs from the classic asset accounting in SAP ERP (ECC) both technically and functionally. Among other things, the goal is integration into the Universal Journal (ACDOCA) as well as a link to the new general ledger.

The New Asset Accounting in S/4HANA

In the “new” asset accounting, current postings are no longer recorded in the existing FIAA totals/transaction tables (ANEP, ANEA, ANLP, ANLC, etc.), but directly in the Universal Journal ACDOCA.

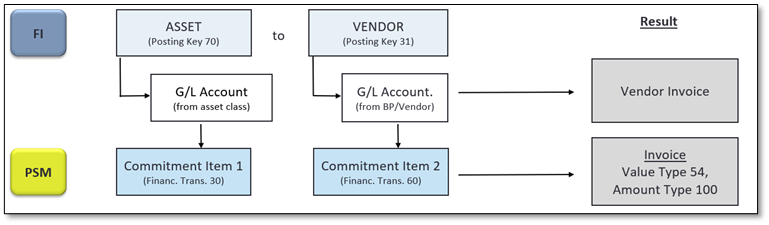

Furthermore, S/4HANA introduces a new posting logic for integrated asset acquisitions: A distinction is made between an operational and a valuation component. While the operational component represents the vendor invoice, an FI document is generated for the valuation component (i.e., capitalization of the asset upon acquisition) in accordance with the applicable accounting regulations.

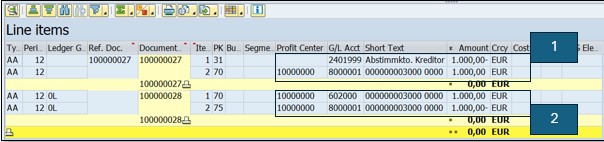

The newly introduced technical clearing account serves as the linking “element” between the operational and valuation parts. For an integrated asset acquisition via transaction F-90, a vendor/creditor and an asset are selected, as before. Upon posting, two FI documents are then automatically generated:

- Operational Part – Vendor Invoice:

Asset (posting key 70 – transaction type 100)

to

Vendor (posting key 31) - Valuation part – Asset:

Asset (Posting Key 70 – G/L Account from Asset Class)

to

Asset (posting key 75 – technical clearing account)

Integration with Budget and Grant Management

SAP Note 2405147 generally recommends that “for consistent budget allocation with active availability control in Budget Management and/or Grants Management […], the same account assignment be derived for the technical clearing account and for the asset reconciliation account. To map different asset account assignments, different technical clearing accounts can be set up depending on the asset class.”

The commitment item to be defined for the technical clearing account should be controlled using financial transaction 30. Since the technical clearing account is also used for the entire procurement chain—from purchase requisition, purchase order, goods receipt, and invoice receipt—the question arises from a budget and grant management perspective as to how the aforementioned consistent updating can be ensured.

Without the technical clearing account, the derivation in Funds Management could previously be mapped as follows:

The correct commitment items were determined using the account assignment derivation tool “FMDERIVE” (Funds Management) from the posted G/L accounts of the asset classes, as well as via the supplier’s reconciliation account or, in Grants Management, via the FI account assignment (maintenance view V_GMFIUPD).

For the new asset accounting and the use of the technical clearing account, there are now different options for deriving the correct commitment items:

Assuming that there should be no difference between the budget and posting objects, the following approaches are available for determining the correct commitment item:

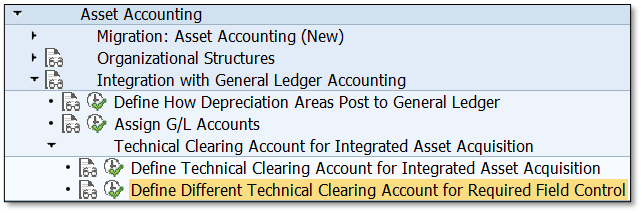

Multiple technical clearing accounts in Asset Accounting

- In Customizing for Asset Accounting, a separate technical clearing account is created for each account determination/asset class.

- The financial positions already used for the corresponding general ledger account of the asset class are stored in the newly created technical clearing accounts.

- Using FMDERIVE, the commitment item is read from the technical clearing account (field CMMT_ITEM) via the function module FMDT_READ_MD_ACCOUNT_COMPANY.

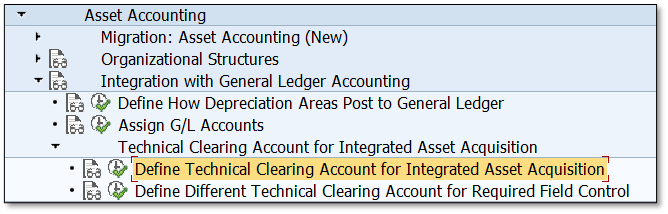

A technical clearing account and differentiation via FMDERIVE

- A technical clearing account is defined in Customizing for Asset Accounting.

- Differentiation of the commitment item by asset class is performed using FMDERIVE

- For example, the function module FMDT_READ_MD_ASSET transfers the Account Determination field (field KTOGR) to the USERTEMP1 field.

- In a further FMDERIVE step of the step type “Derivation Rule,” the commitment item (target field COMMIT_ITEM) is derived from the source fields G/L Account (ACCOUNT_NUMBER) and USERTEMP1 (=Account Determination) via rule steps to be maintained.

This ensures correct updating and budget consumption in both cases:

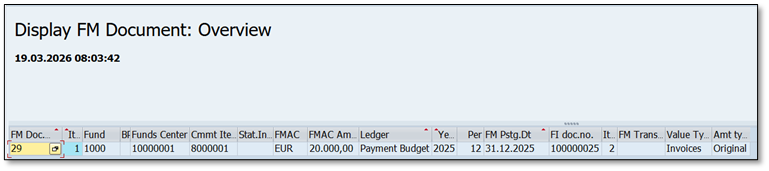

Operational part of the asset acquisition from a budget perspective

The acquisition has been correctly updated in the budget as an open invoice, value type 54, amount type 0100.

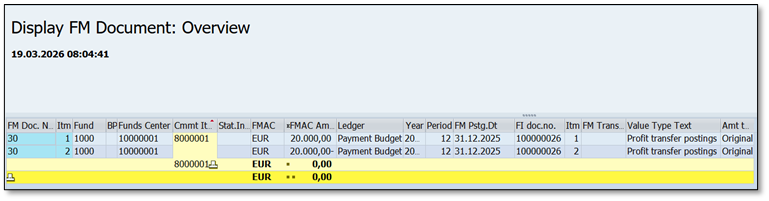

Valuation part of the asset acquisition from a budget perspective

The valuation portion is a transfer posting (value type 66) to identical account assignments and is therefore budget-neutral in Funds Management.

Without this type of derivation, the follow-on document for the valuation portion might be posted to different commitment items in Funds Management. This, in turn, leads to incorrect budget consumption, as shown in the following PSM document:

For correct updating in Grant Management (GRANTEE), the new technical clearing accounts must be configured in Update Control (V_GMFIUPD) in the same way as the existing asset ledger accounts.

In this case, both the asset inventory account and the technical clearing account are set to value type 99 and true posting, so that the update and budget consumption occur correctly on output type 0830:

Alternatives

If you wish to avoid setting up additional clearing accounts in Asset Accounting or adjusting the “FMDERIVE” derivation, you can use the following alternative approaches to at least ensure that budget consumption in Funds Management occurs on a central commitment item:

- Use of a budget structure and working with commitment item hierarchies: If the budget structure is used in Funds Management, the “Define derivation strategy for budget account assignments” available there, in conjunction with, for example, commitment item hierarchies, can be used to derive a central, budget-carrying commitment item.

- Using the Derivation Strategy for AVK Control Objects: This option simply employs an availability control derivation strategy to determine the budget object from financial positions posted for Active Availability Control (AVK). Neither the derivation of the budget structure plan nor the use of hierarchies is required for this.

CONCLUSION

Although the last two alternatives mentioned may seem simpler at first glance, when integrating the new Asset Accounting with Budget and Third-Party Fund Management, you must always consider what your specific requirements for updating data are. In my opinion, to ensure consistent mapping of the correct value types to the various commitment items, it is necessary to understand the processes in Asset Accounting and to use appropriate derivation steps to ensure that updates to Budget and Third-Party Fund Management occur consistently.

And this is exactly where we are always available to assist our customers with advice and support on all technical and business-related questions regarding budget management and integration. Get in touch with us!