Spain is aggressively driving the digitization of its economy. The focus is on two major goals: combating tax fraud and reducing late payments in business transactions. For companies operating in Spain, this means far-reaching regulatory changes to their invoicing processes.

In this article, we’ll walk you through the complex Spanish regulatory landscape, outline the applicable timelines, explain how connectivity (keyword: providers) is regulated, and show why SAP Document and Reporting Compliance (DRC), combined with our expertise at adesso business consulting, is the optimal solution for you.

Spain is clearly moving toward mandatory digital B2B communication for e-invoicing. For companies, one thing is particularly crucial: Not only are the regulations becoming more concrete, but so is the technical target state. Between the established B2G requirement, new B2B regulations, and the separate VERI*FACTU system for invoicing systems, a market is emerging in which structured invoices, status messages, payment information, and platform connectivity must all work together.

Key points at a glance

- E-invoicing for B2G has been established in Spain since 2015, via FACe and the Facturae format.

- For B2B, Real Decreto 238/2026 (“the Royal Decree”) establishes the regulatory framework; the effective start dates depend on the ministerial ordinance regarding the public solution and are currently being drafted.

- Based on the current draft, a rollout starting October 1, 2027, or October 1, 2028, is realistic, but this can only be confirmed once the decree is finally adopted.

- An external provider is not legally required, as a public, free solution is planned; however, from an operational standpoint, a private platform often makes sense.

Regulatory Framework: Clearly Distinguishing Three Levels

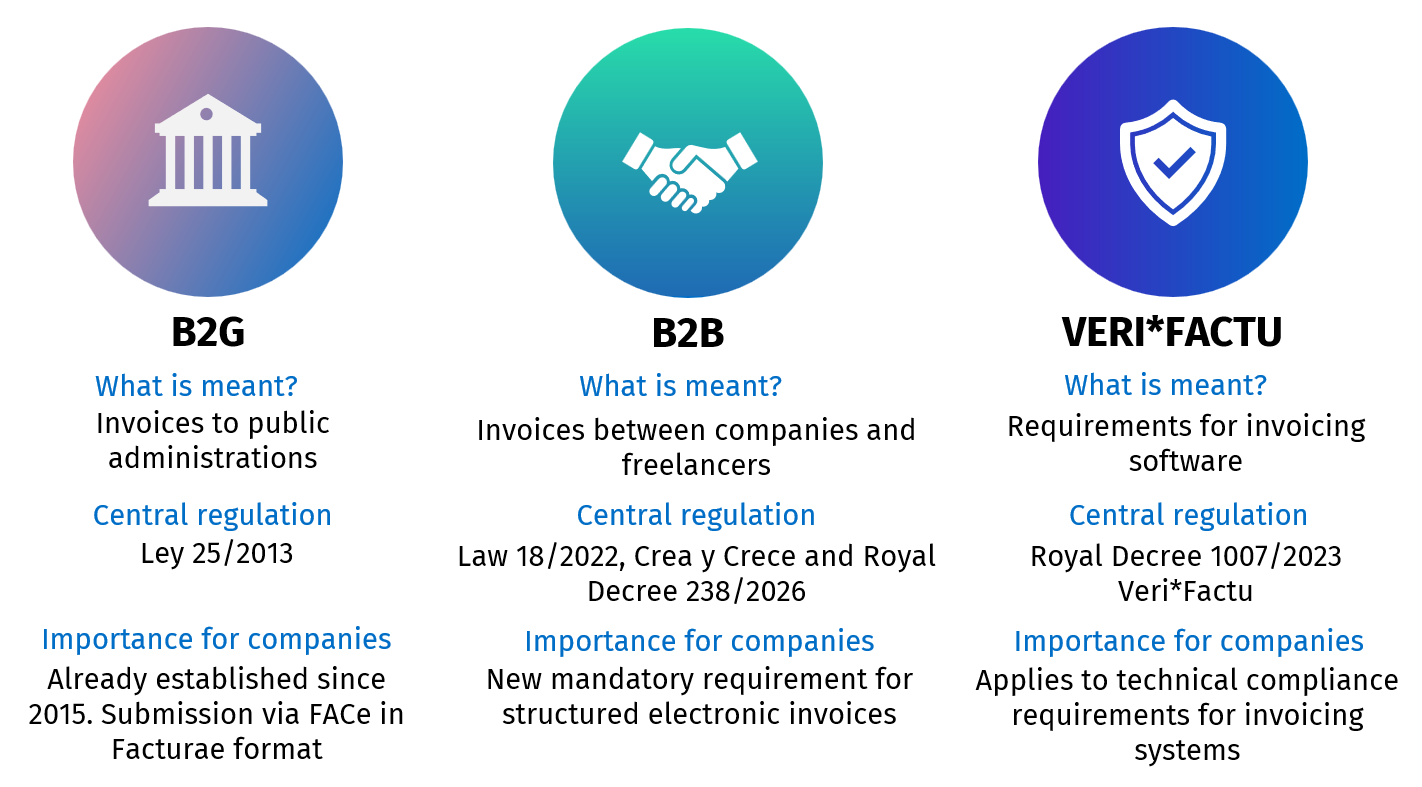

When discussing e-invoicing in Spain, it is important to first distinguish between three levels: B2G, B2B, and VERI*FACTU. They are all related to invoices but govern different aspects.

B2G refers to invoices sent to public administrations. This requirement has been in place in Spain since 2015 under Ley 25/2013. Invoices sent to public entities are processed electronically via gateways such as FACe and transmitted in the structured Facturae (XML) format to the relevant accounting office. Spain thus already has practical experience with electronic invoices, government infrastructure, and digital audit processes.

However, the real new focus is on the B2B sector. Ley 18/2022, known as Crea y Crece, requires businesses and freelancers to use electronic invoices when transacting with one another. Real Decreto 238/2026 specifies the technical and organizational details of this system. This involves not only sending a digital invoice but also ensuring transparency throughout the entire invoice lifecycle: acceptance, rejection, due date, and payment are all part of the regulatory framework.

VERI*FACTU is a separate matter. This system is based on Royal Decree 1007/2023 and does not concern the exchange channel between companies, but rather the requirements for invoicing software. The focus is on the integrity, traceability, and immutability of invoice records. For companies, this means that Spain requires not only e-invoicing connectivity but also software compliance.

What Real Decreto 238/2026 Specifies

Real Decreto (RD) 238/2026 specifies the Spanish B2B framework for mandatory electronic invoicing between businesses and self-employed individuals. The requirement applies in particular to cases where the receipt of the invoice is anchored in Spain – for example, through a registered office, permanent establishment, domicile, or habitual residence. This translates the general legal mandate from Crea y Crece into a more concrete regulatory framework.

A key point is the invoice format. Electronic B2B invoices must be structured and comply with the European semantic data model EN 16931. Accepted formats include UBL, CII, EDIFACT, and Facturae. This makes it clear that Spain is not relying on simple PDF invoices, but rather on machine-readable invoice data that can be processed, verified, and reused by systems.

Furthermore, Real Decreto 238/2026 broadens the scope to encompass the entire invoice lifecycle. Invoice recipients must not only receive the invoice but also provide certain status information. This includes, in particular, the commercial acceptance or rejection of the invoice, as well as information regarding full actual payment. Payment must be reported, including the effective payment date and the due date.

Under RD 238/2026, the deadline for reporting full payment is generally a maximum of four calendar days from the effective payment date, excluding Saturdays, Sundays, and national holidays. This short reporting deadline follows a logic already familiar in Spain: Under the Suministro Inmediato de Información (SII) system, certain VAT invoice data is already transmitted to the Spanish tax authority, the AEAT, in near real time – also within a four-day deadline. As a result, e-invoicing in Spain is not just a matter of invoice format, but also a matter of process and data quality: acceptance, rejection, due date, payment, correction, and monitoring must be consistently tracked.

VERI*FACTU: important, but not to be confused with B2B e-invoicing

VERI*FACTU is not a mandatory B2B e-invoicing platform, but rather a compliance mechanism within the Spanish regulatory framework for Sistemas Informáticos de Facturación (SIF). This framework addresses the technical reliability of the invoicing software used: invoice records must be generated in a way that ensures they are traceable, tamper-proof, storable, and verifiable. B2B e-invoicing governs the structured exchange and reporting of invoice-related information. SIF/VERI*FACTU governs the requirements for the system that generates and secures the invoice records. For SAP projects, therefore, both topics should be considered together, but clearly separated from one another in both business and technical terms.

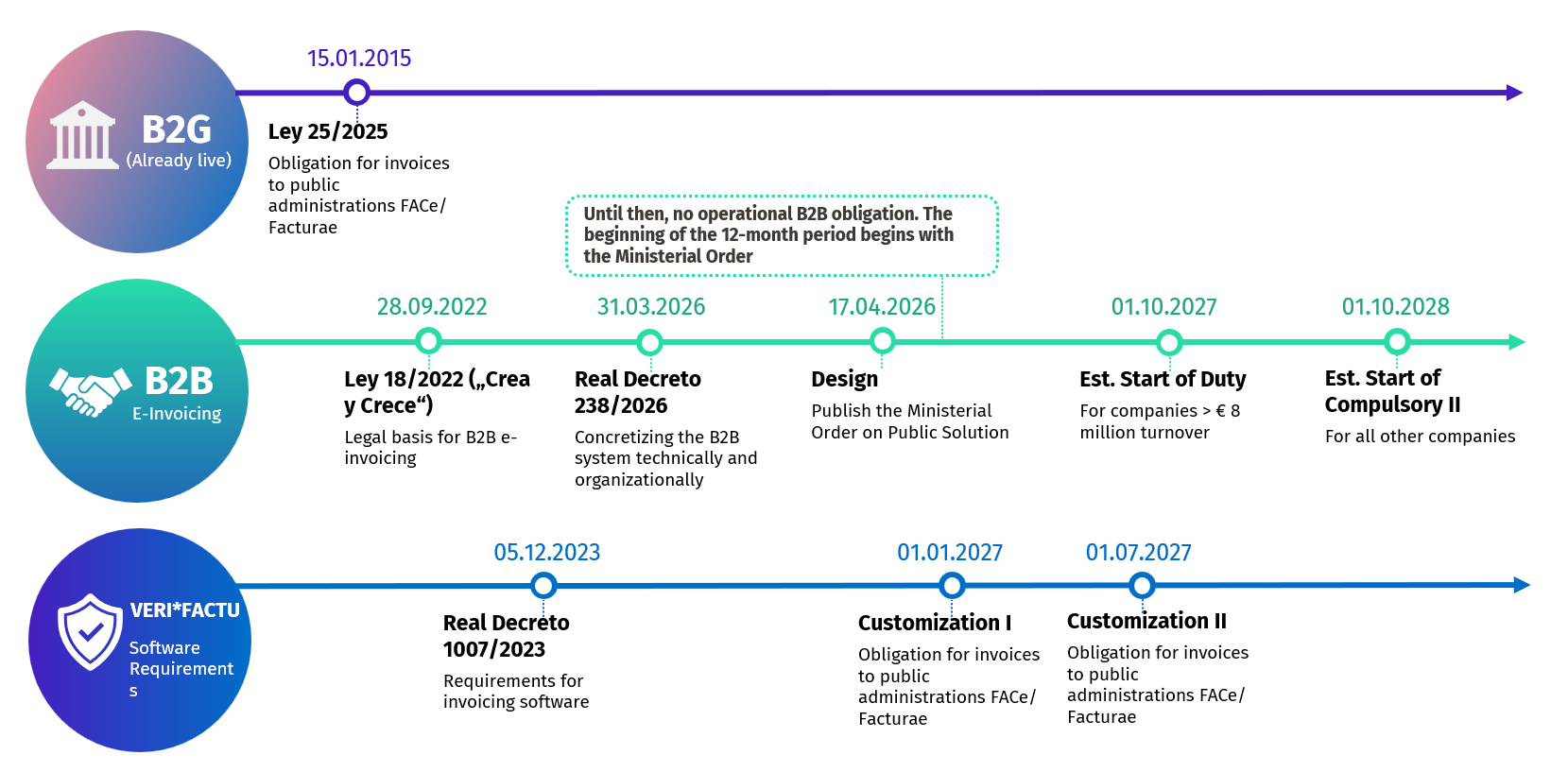

Timeline: What is certain, and what is still a draft?

For project planning, it is crucial to distinguish between the applicable legal framework and the ministerial ordinance, which has not yet been finalized.

RD 238/2026 has been published, but its effective implementation is contingent upon the regulations governing the public solution. The draft ministerial ordinance provides for entry into force on October 1, 2026. Based on the logic of Ley 18/2022 and information from the Spanish Tax Agency (AEAT), this results in a phased rollout: twelve months later for companies with prior-year revenue exceeding 8 million euros, and 24 months later for all other entities. Therefore, October 1, 2027, and October 1, 2028, respectively, are plausible working assumptions – but only the final adoption of the law will make these dates reliable.

Connectivity: Is a provider mandatory in Spain?

The short answer is no – at least not legally required. Spain explicitly provides for a public, free solution.

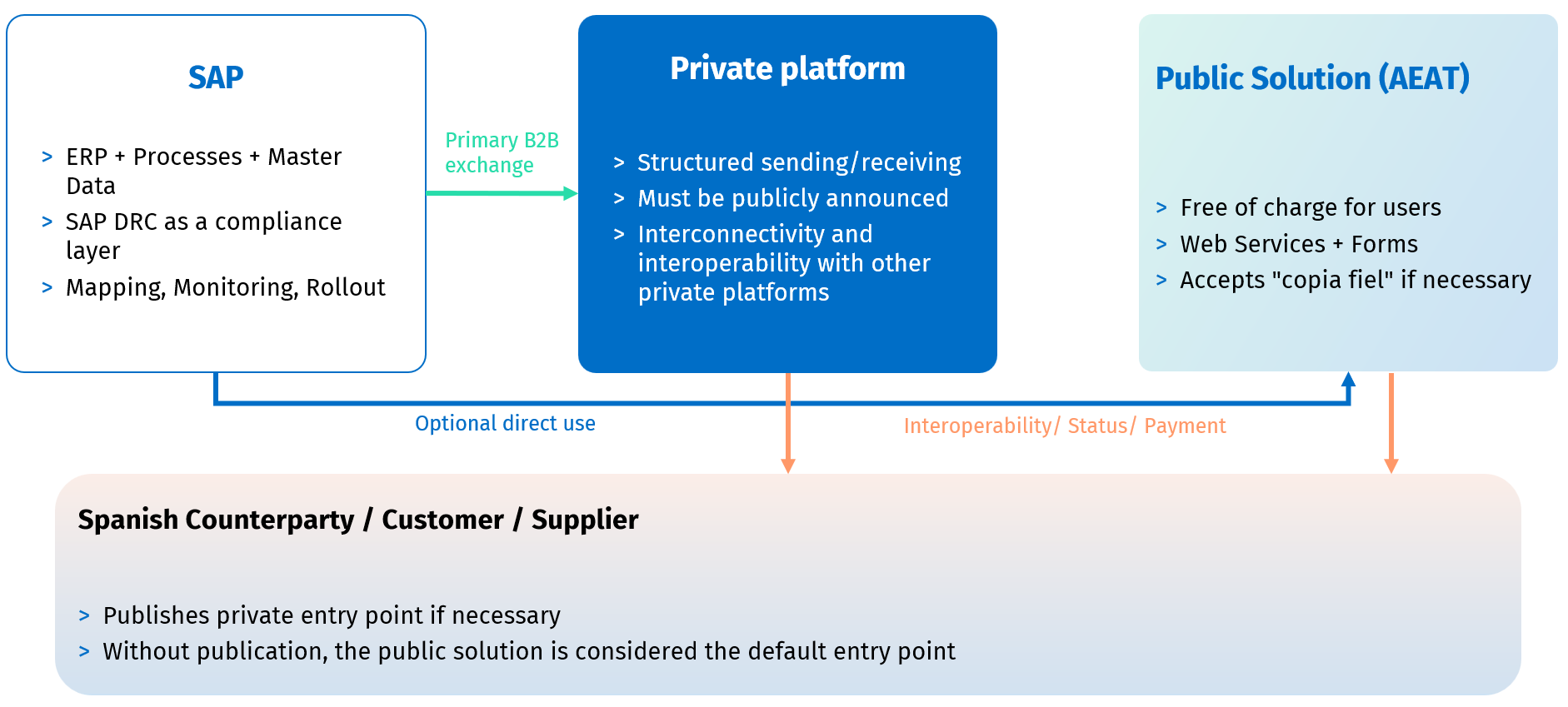

The figure illustrates the core connectivity logic of the Spanish B2B model: An external provider is not legally required because Spain provides for a public, free AEAT solution. Companies can therefore exchange structured B2B invoices via private platforms, directly through the public solution, or using a combination of both methods.

However, this does not mean that private platforms are unimportant. Real Decreto 238/2026 requires private platforms to ensure interoperability and interconnectivity. Anyone using a private entry point must publicly disclose it. If this is not done, the public AEAT solution automatically serves as the default entry point. The public solution thus functions not only as a direct exchange channel but also as a fallback and bridging mechanism.

From a technical implementation perspective, this means that Spain is not simply a matter of “PDF plus transmission.” Invoices must be transmitted in a structured format; according to the current draft, the public solution uses UBL as well as web services and forms. Companies that do not send invoices directly via the public solution must additionally submit an electronic “copia fiel” (certified copy of the original invoice) to the public solution.

From a project perspective, the question of which provider to use should therefore be addressed not only from a legal standpoint but also from an architectural one: An external provider is not strictly necessary but can be very useful for scaling, routing, monitoring, onboarding, and international e-invoicing scenarios. Large companies can, in principle, use the public AEAT solution. In practice, however, the public solution may reach its limits when dealing with complex SAP/ERP landscapes, high invoice volumes, multiple subsidiaries, international formats, and requirements for monitoring, partner onboarding, and multi-country capability. Companies will therefore often use private platforms in addition to or as an alternative to the public solution, as these enable greater operational scalability, integration, and automation.

Why This Is Particularly Relevant for SAP Companies

In SAP landscapes in particular, Spanish regulations very quickly turn into an integration project. It is not enough to simply generate structured outgoing invoices. Rather, companies must ensure end-to-end that formats, recipient channels, status messages, payment information, and monitoring work together reliably. This is precisely where SAP Document and Reporting Compliance (SAP DRC) becomes strategically relevant.

For SAP customers, this enables the creation of a central compliance layer that does not treat the regulatory framework as an isolated, ad-hoc solution, but rather embeds it into the existing ERP and financial architecture. From adesso’s perspective, this is the natural starting point: understand the regulatory framework, define the target state, integrate SAP DRC seamlessly, establish connectivity with a public solution or private platform, and reliably transition the scenario into production. Precisely because Spain is implementing B2G, B2B, and software-related obligations in parallel, a structured SAP implementation is much more than mere format conversion.

Anyone who views Spain merely as a new country-specific requirement underestimates the operational depth involved. Conversely, those who address the issue early on through SAP DRC and a clear connectivity strategy reduce friction later on during rollout, as well as within business units and IT. You can read here why e-invoicing is more than just an IT project.

Conclusion: Spain is no longer a latecomer, but a concrete transformation project

Spain is currently demonstrating very clearly how quickly general legal expectations can become a concrete implementation reality. B2G has been in place for years. B2B now has a clear regulatory foundation with Real Decreto 238/2026. The final piece of the puzzle still pending is the ministerial ordinance on the public solution, and that is precisely why companies should not wait for perfect clarity now, but rather prepare their target vision, data quality, and SAP or platform architecture.

As an SAP partner, adesso business consulting supports companies in integrating SAP DRC into existing ERP and financial architectures and in seamlessly implementing regulatory requirements such as B2B e-invoicing, status notifications, and connectivity. You can read about exactly how implementation works with SAP-DRC in another blog post here. At adesso business consulting, we understand the specifics of the Spanish market—from the SIF/VERI*FACTU regulations to the provider model under the Ley Crea y Crece and the Suministro Inmediato de Información (SII). Everything from a single source: We seamlessly integrate SAP DRC into your existing system landscape.

- Secure connectivity: We set up the architecture so that you can flexibly decide whether to use direct interfaces to the AEAT (for the “copia fiel”) or connect to Peppol or EDI networks.

- Automation: We handle the 4-day deadline for payment status reports via automated workflows directly from your SAP Financials system.

With adesso business consulting and SAP DRC, you can turn Spanish e-invoicing regulations from an IT risk into a predictable, automated process. Contact us to get your systems ready in time for 2027.